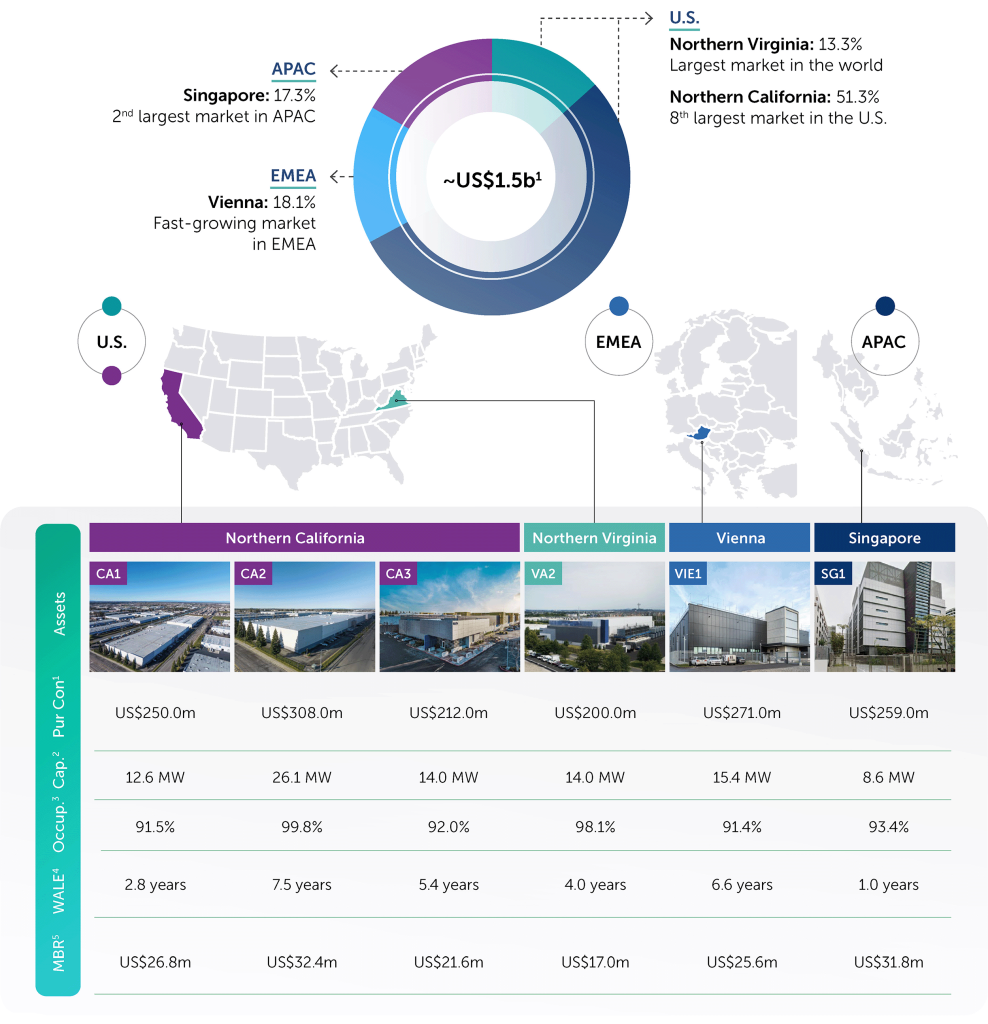

Portfolio strategically diversified across key global markets, including top ten markets in the U.S. and APAC

Our portfolio is diversified across key data center markets in North America, EMEA and APAC, consistent with the Sponsor’s operational footprint. This enables NTT DC REIT to leverage the Sponsor’s familiarity and expertise in managing and operating data centers in these markets, particularly as the Sponsor continues to provide property management services to the assets in the portfolio.

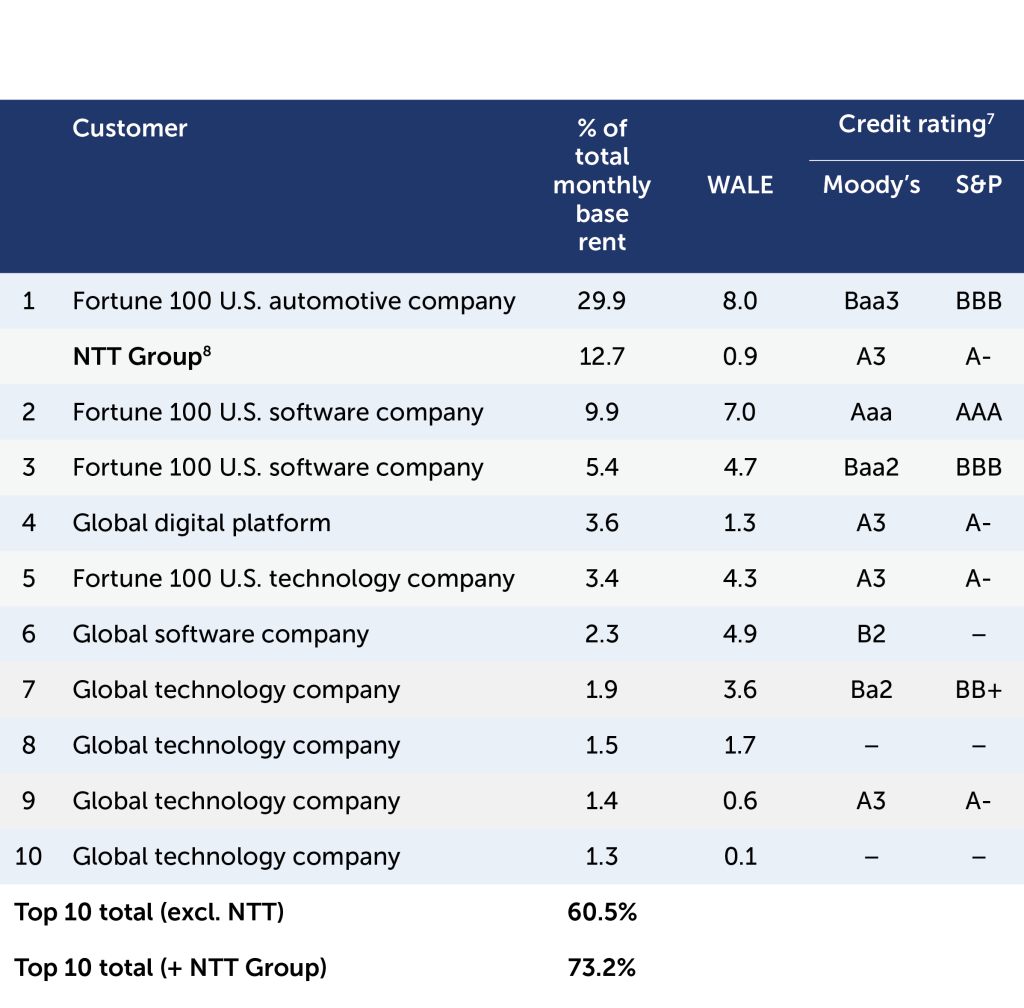

Diverse customer base anchored by leading global enterprises with high credit quality

Our Portfolio

| Asset | Location | Land tenure expiry | Year of RFO / last refurbishment7 | Design IT load (MW) | No. of customers | Occupancy (based on design IT load) (%) | Annualised MBR (US$m) | WALE (years) | Purchase Consideration (US$m)1 | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| U.S. | ||||||||||||||

| VA2 | 44610 Guilford Dr., Ashburn | Freehold | 2016 / 2024 | 14.0 | 9 | 98.1% | 17.0 | 4.0 | 200 | |||||

| CA1 | 1200 Striker Ave., Sacramento | Freehold | 2001 / 2025 | 12.6 | 121 | 91.5% | 26.8 | 2.8 | 250 | |||||

| CA2 | 1312 Striker Ave., Sacramento | Freehold | 2011 / 2025 | 26.1 | 22 | 99.8% | 32.4 | 7.5 | 308 | |||||

| CA3 | 1625 W. National Dr., Sacramento | Freehold | 2015 / 2024 | 14.0 | 31 | 92.0% | 21.6 | 5.4 | 212 | |||||

| EMEA | ||||||||||||||

| VIE1 | Computerstrasse 4, 1100 Vienna | Freehold | 2023 / - | 15.4 | 76 | 91.4% | 25.6 | 6.6 | 271 | |||||

| APAC | ||||||||||||||

| SG1 | 51 Serangoon North Ave. 4 | Aug 2040 (+30y option)8 | 2012 / 2024 | 8.6 | 27 | 93.4% | 31.8 | 1.0 | 259 | |||||

| Total / Average / Weighted Average | 90.7 | 2629 | 95.1% | 155.2 | 4.4 | 1,500 | ||||||||

| 1 | Based on IPO Purchase Consideration. |

| 2 | Design IT load capacity. |

| 3 | Contracted IT capacity divided by total design IT capacity. |

| 4 | Weighted by total monthly base rent. |

| 5 | Annualised monthly base rent. |

| 6 | Credit rating of the parent group if available, as of 30 September 2025. |

| 7 | RFO: Ready-for-Occupancy date, Last refurbishment: Refers to the completion of projects where infrastructure supporting at least 15% of operational capacity has been replaced. |

| 8 | Occupational lease of land with JTC, paid in full until August 2040 which is the initial term of the lease with JTC, with an option for a further 30-year term until 2070 subject to the fulfilment of certain conditions under the lease. The conditions for a further 30-year term until 2070 include: (i) the tenant making a fixed investment of at least SGD 35,000,000 on SG1 during the initial lease term, (ii) the gross plot ratio of the site being not less than 2.47 but not more than 2.50 and (iii) at the expiry of the initial lease term there being no existing breach or non-observance of any of the tenant’s obligations. JTC have confirmed in writing that conditions (i) and (ii) have been satisfied and that, in relation to (iii), there are currently no known breaches. |

| 9 | Only unique customer names are counted for customers located in the U.S. |