Key Investment Highlights

The Manager believes that an investment in NTT DC REIT offers the following benefits to unitholders:

1. Significant growth in the global data center market with further headroom for expansion

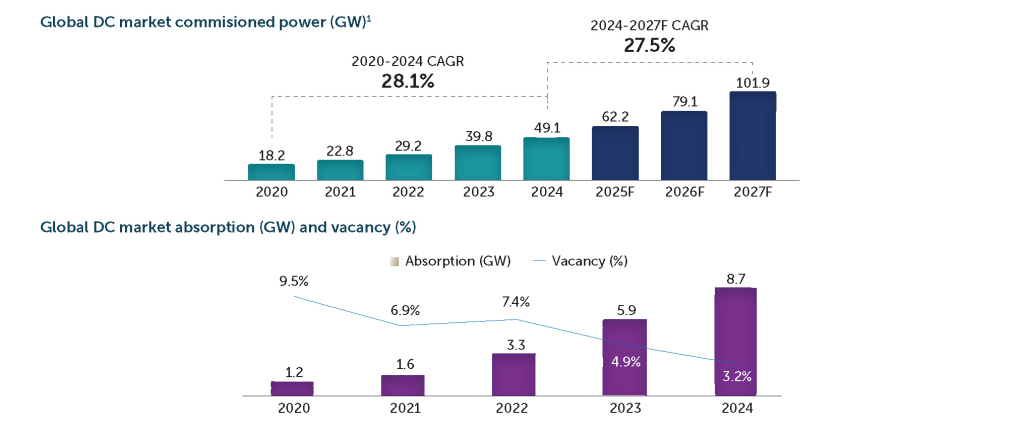

- The global data center market has demonstrated sizeable growth underpinned by scalable, long-term demand drivers

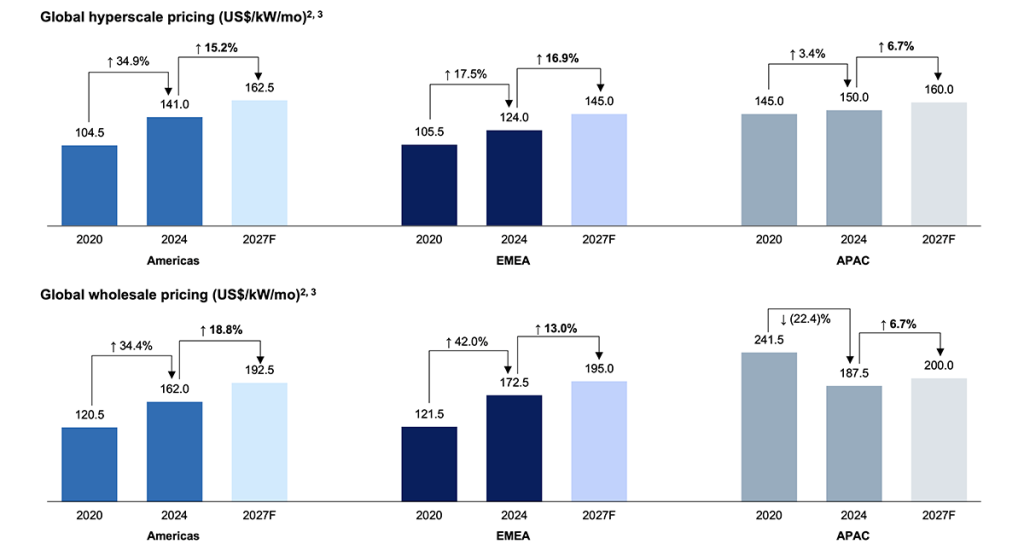

- Consistent growth in data center pricing globally, alongside increasing capacity absorption and declining vacancies

- Surge of capital allocation into data centers alongside increasing demand and consistent pricing growth

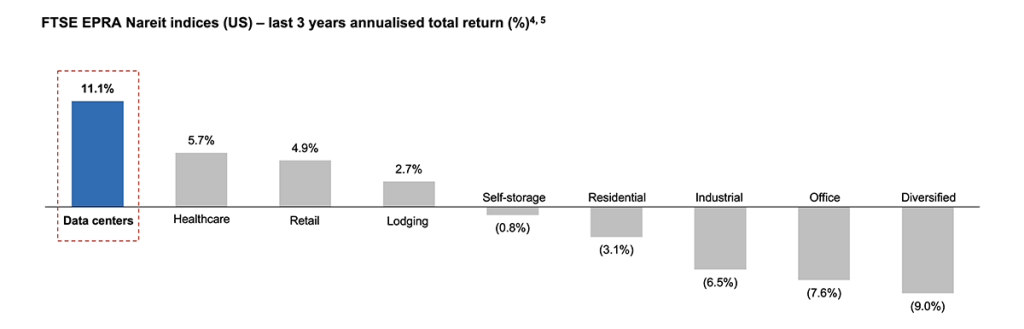

- Data centers have delivered the highest total return compared to other major traditional real estate classes over the last three years

2. Unfettered access to and support from a leading, global Sponsor with clear alignment of interests

- NTT Limited (the “Sponsor”) is part of the NTT Group, a major global IT services and telecommunications group with a leading global data center business

- NTT DC REIT and the Sponsor may benefit from access to potential synergies with the broader NTT Group, including its global connectivity infrastructure and next-generation technologies

- Clear alignment of interests between the Sponsor and NTT DC REIT

3. Premium-quality portfolio with high specifications, diversified across key data center markets globally

- Portfolio comprises high quality assets with stringent operational and technical specifications that serve customers’ high-value workloads

- Assets strategically diversified across key data center markets globally, including top 10 markets in the U.S. and APAC

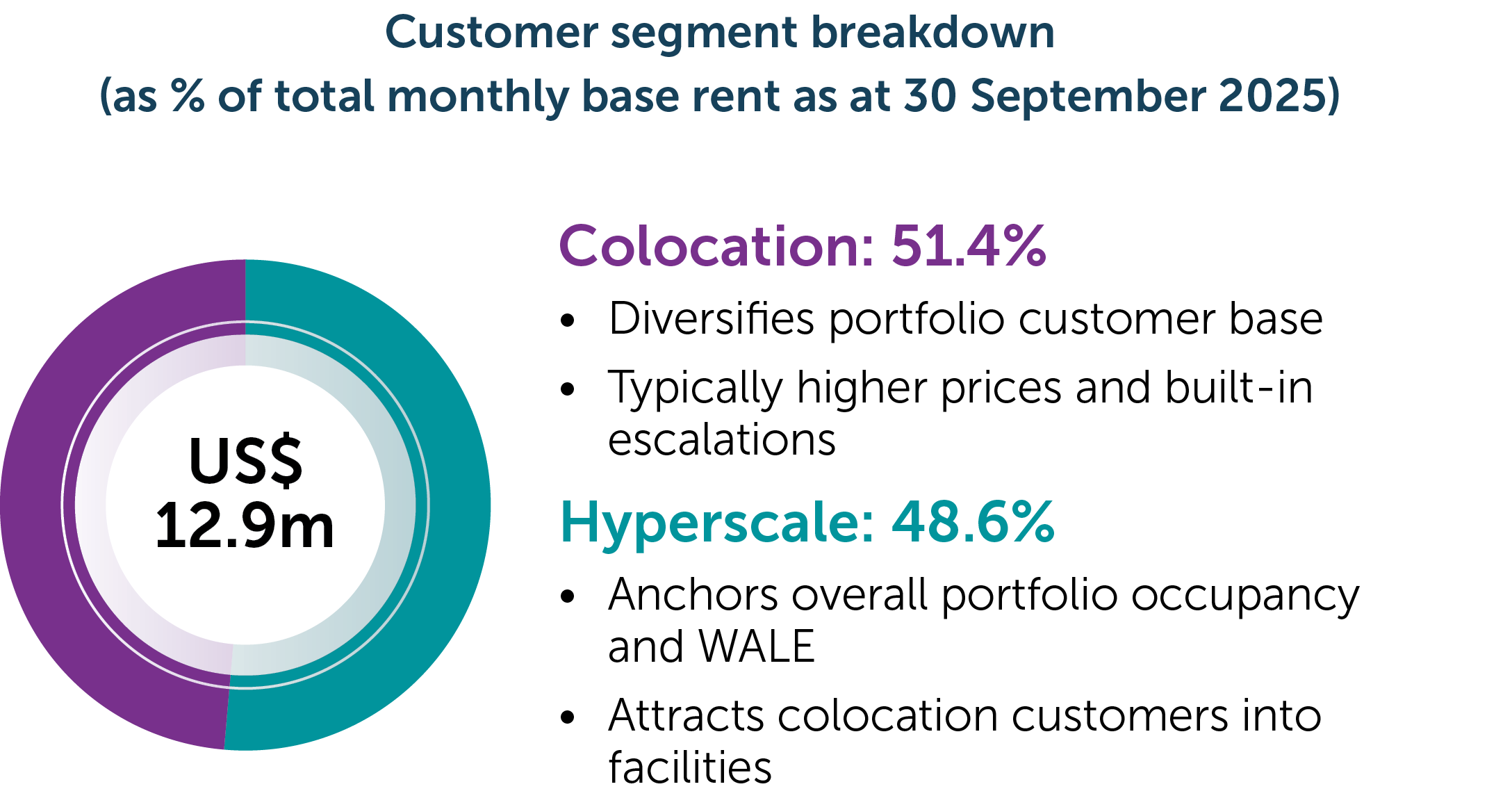

4. Robust income generation capability underpinned by diverse base of premier customers and organic growth drivers

- Optimal mix of hyperscale and colocation customers in the portfolio supports strong occupancy and pricing growth

- Diverse customer base anchored by leading global enterprises with high credit quality

- Organic growth from contractual pricing escalations with further upside from strong reversionary potential

- Potential earnings uplift from asset enhancement initiatives

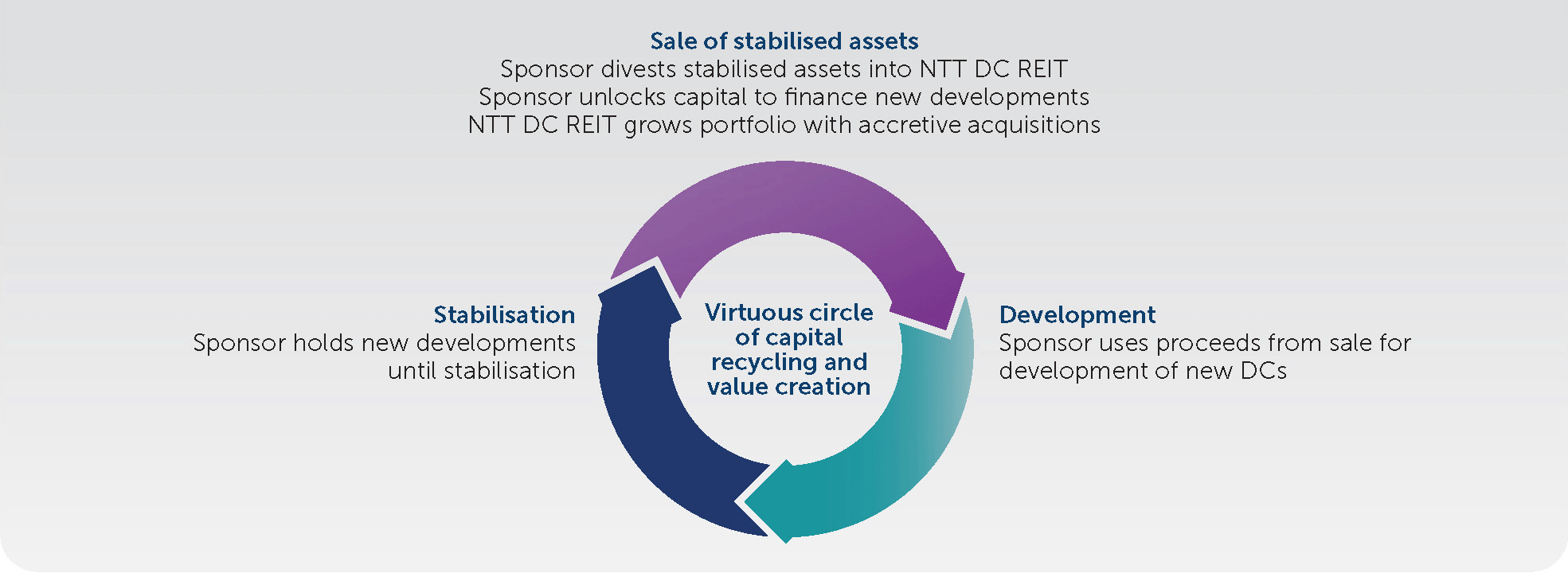

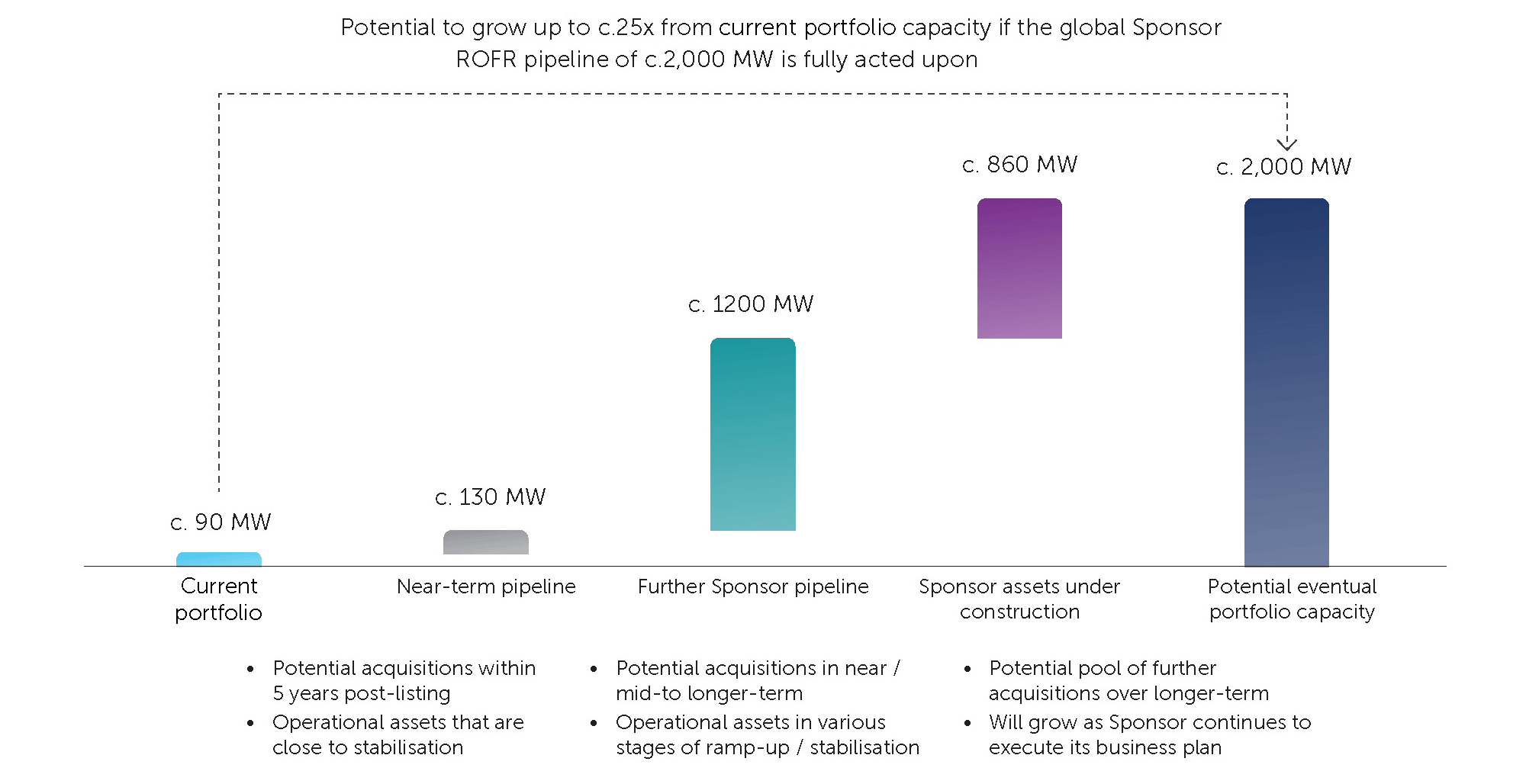

5. Extensive pipeline of acquisition-led growth opportunities from the global Sponsor Right Of First Refusal (“ROFR”)

- Access to Sponsor pipeline of over 2,000 MW6, of which approximately 130 MW represents identified pipeline for near-term acquisition

6. Robust capital structure and active capital management to facilitate future growth

- Low day one gearing of 35.0% provides financial flexibility to pursue future acquisitions

- Prudent capital management and hedging strategy with proactive interest rate and FX risk management

- Well-staggered debt expiry profile, with no debt expiry in the next three financial years to FY27/28

7. Extensively experienced management team and Board of Directors with deep domain expertise

- Veteran management team with strong track record in managing investments and operations in real estate and data centers

- Accomplished Board of Directors with extensive experience and diverse expertise

| 1 | Based on colocation and hyperscale commissioned power. |

| 2 | Prices indicated refer to the mid-point of the maximum and minimum prices for each region, provided in the Independent Market Research Report. |

| 3 | US$/KW/mo refer to prices in US$ per kilowatt per month excluding power costs. |

| 4 | The FTSE EPRA Nareit Index tracks the performance of listed REITs and real estate companies in the U.S., comprising 104 REITs/companies. The index is further broken down into property sub-sectors as shown in the chart above. The last three years’ total return of each constituent REIT/company is calculated as the sum total of the dividends received per share/unit and the capital appreciation of each share/unit over the last three years, divided by the share/unit price at the start of the three-year period. |

| 5 | Data retrieved: January 2025. |

| 6 | As at 31 December 2024. The Sponsor ROFR pipeline excludes data center properties held under joint ventures where a minority stake is held by the Sponsor Group which amounts to approximately 200 MW of IT capacity. |